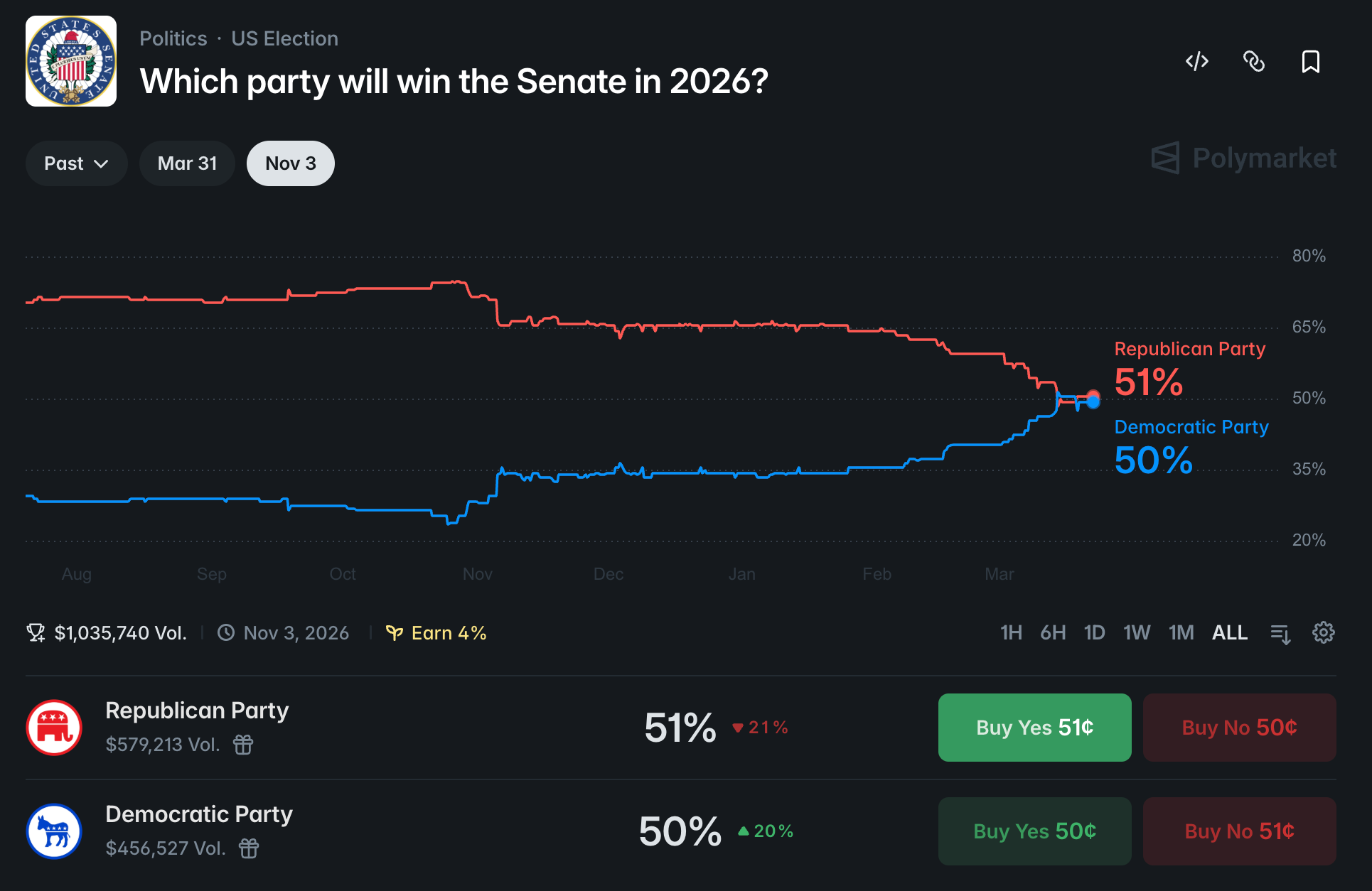

Into the Dem sweep midterm

summary for ACA & IRA revival beneficiaries

Trump losing midterm & Dem sweep becomes the most likely outcome with Hormuz crisis. So what would be the thematic trade into this outcome? The biggest policy under Trump has been ACA credit expiry and IRA credit cut. When Dem takes the seat back, they likely try to roll back these credit.

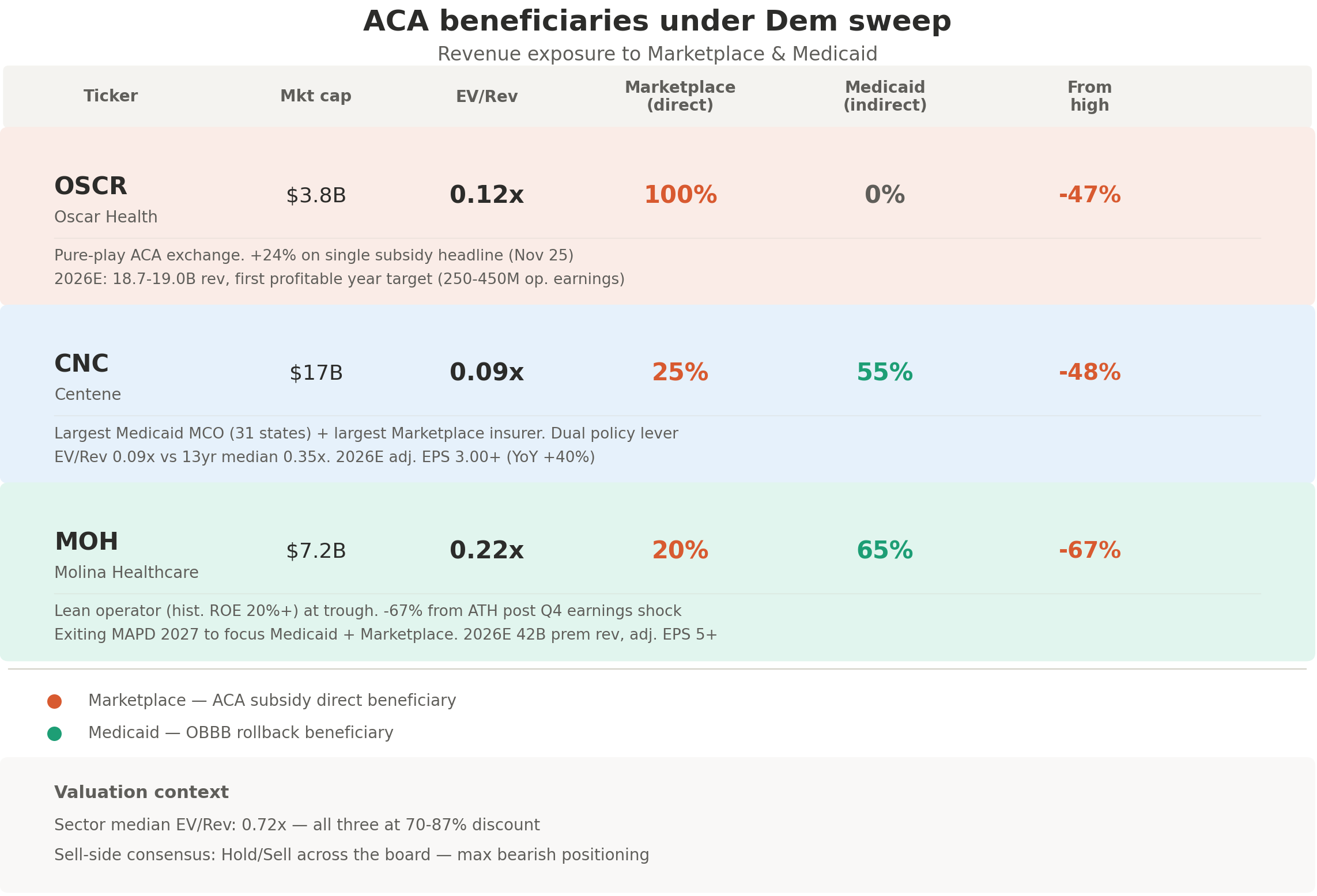

ACA beneficiaries:

Since 2024 presidential election, all the healthcare insurers are killed. UNH -55%, ELV -45%, etc. show the how conditions were bad to insurers under Trump. It can be reversed with the midterm catalyst. Chart below shows the revenue exposure to Marketplace and Medicaid, which are healthcare policy priority for Dems.

OSCR is the ACA pure play insurer, getting 100% revenue from 2 million individual exchange plan. 2026 guidance is $19B revenue with $250-450M operating profit. Stock moved +23% with a subsidy headline in November 2025, showing OSCR has the biggest convexity to ACA credit reversal. Sell rating from Wells Fargo.

CNC is the largest ACA marketplace participants 3.5 million members, and also largest Medicaid operator, with 25.1 million members. Dem sweep will provide the biggest absolute dollar revenue boost for CNC. Also, EV/revenue at 0.09x is much lower than its 13y median of 0.35x, hovering at all time low. Hold rating with relentless target cut from JP Morgan.

MOH is the Medicaid-focused operator with 20% marketplace. Management states 2026 being the trough year with EPS $5. Under Dem sweep, it can get dual catalyst for ACA and Medicaid side, with higher upside from the market cap perspective. After Q4 revenue & guidance shock, many sell side reports cut the ratings and target.

For ACA marketplace credit, Dem already passed it with 230-196 in GOP dominant House. Under Dem sweep narrative, the market will price ACA credit extension or even permanent credit. For Medicaid, Trump passed OBBB to cut big portion of financing. Accordingly, Dem will try to roll back medicaid spending after they get House and Senate.

Another bonus point: If we have prolonged Hormuz war followed by recession, defensive basket including healthcare would get idiosyncratic bid. Considering insurers are crushed in terms of valuation under Trump, it can have explosive effect into the sluggish economy and market to find safe heaven.

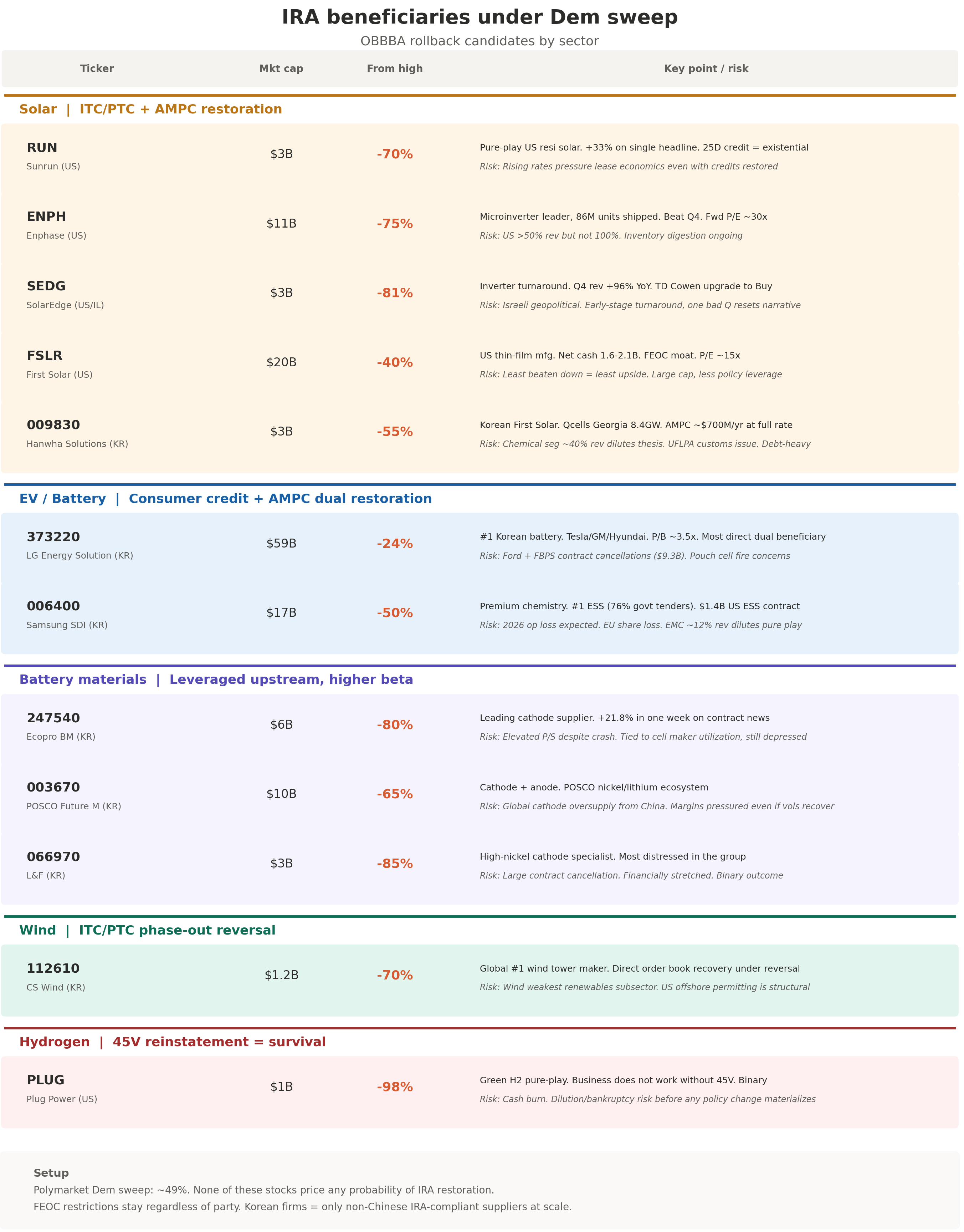

IRA beneficiaries: the second leg of the Dem sweep trade

OBBBA killed ~60% of IRA credits. EV tax credits, residential solar credit, wind credit, and hydrogen credits are dead already or fading to dead by 2028. Unlike ACA where the beneficiary pool is narrow (three managed care names), IRA restoration has a much wider surface area.

Solar: Hardest hit under OBBB

RUN is the pure-play US residential solar installer. 30% residential credit (25D) is the backbone of its lease model, without it the business doesn’t work. Stock moved +33% on a single Treasury guidance headline in Aug 2025, showing max convexity to credit reversal.

ENPH is the microinverter leader with 86M units shipped. Better business than RUN with international diversification, but US is still >50% of revenue. Beat Q4 ($0.71 vs $0.58 est). Inventory digestion still ongoing.

SEDG is mid-turnaround. Q4 rev +96% YoY, TD Cowen upgraded to Buy. IRA restoration is additional optionality. Still very early though, and Israeli geopolitical adds noise.

FSLR is US thin-film manufacturing, net cash $1.6-2.1B, FEOC moat protects regardless of party. Only down 40% from high while others are down 70-80%.

009830 (Hanwha Solutions) is the Korean FSLR. Qcells operates the largest non-Chinese solar manufacturing in the US (Georgia, 8.4GW). AMPC ~$700M/yr at full run-rate. Chemical segment is ~40% of revenue so not a clean solar pure-play, and UFLPA customs issue hit Georgia operations, with debt-heavy balance sheet issue.

EV & battery: Korea is the biggest winner for IRA

373220 (LG Energy Solution) is Korea’s #1 battery, supplying Tesla/GM/Hyundai. Gets both consumer credit and AMPC back if restored. AMPC is literally the only thing keeping this profitable.

006400 (Samsung SDI) has the strongest ESS positioning among Korean Big 3 (76% of govt ESS tenders). Secured $1.4B US ESS contract. EMC segment (~12% rev) means it’s not a clean battery play.

Battery materials. Leveraged upstream, higher beta.

247540 (Ecopro BM) is the leading cathode supplier. Surged 21.8% in one week on contract news alone. Still trades at elevated P/S despite 80% drawdown. Revenue entirely tied to cell maker utilization which remains depressed.

003670 (POSCO Future M) is cathode + anode, plugged into POSCO nickel/lithium supply chain. Global cathode oversupply from China. Margins may not recover even if volumes do.

066970 (L&F) is the most distressed name in the group. High-nickel cathode specialist, large contract cancellation, financially stretched.

Wind & Hydrogen

112610 (CS Wind) is global #1 wind tower maker. ITC/PTC reversal directly refills order book. Wind is the weakest renewables subsector though. US offshore permitting bottlenecks are structural, not just policy.

PLUG is green hydrogen pure-play. Business does not work without 45V. Cash burn raises real dilution/bankruptcy risk before any policy change materializes.